MicroStrategy has purchased an additional 5,050 bitcoins for ~$242.9 million in cash at an average price of ~$48,099 per #bitcoin. As of 9/12/21 we hodl ~114,042 bitcoins acquired for ~$3.16 billion at an average price of ~$27,713 per bitcoin.

Category: Investment Discussions

Visa’s 54 Bitcoin-Linked Cards Pave The Way For Younger Generations To Spend Growing Crypto Wealth

These projects have gained traction — crypto-linked Visa debit cards facilitated over $1 billion worth of transactions across Visa’s 70 million merchants worldwide in the first half of 2021 alone.

CZ, the CEO of Binance, Talks with Bloomberg about Binance and Crypto’s Future

For years I have been listening to CZ. He is one of the more astute people in the Crypto world. He additionally cares deeply about doing good for humanity. He is reasonable in working with regulators and describes in this interview, in a discussion format that is like sitting on the couch in a casual conversation, insights that are critical to the maturity and adoption of this new asset class that is being built on incredible technology.

50 Years After Going Off Gold, the Dollar Must Go for Crypto

This is a fascinating article from Bloomberg. If you do not want to read the history section, skip about half-way down in the article, but to be honest the entire editorial is a worthwhile read. The below extract is spot on!

As Harold James says, we are living through a monetary revolution as profound as the one that swept away the remains of the gold standard. But there is a difference. In the 1970s and 1980s, the attempts by governments to regulate the revolution were swept away. Nixon’s price and wage controls were an abject failure, just as the economist Milton Friedman (and Shultz) had foreseen. Under Reagan, it was deregulation that enabled American financial institutions to become the dominant players in international markets.

The winners of my boyhood have become the bloated incumbents of my middle age. The innovative energy has passed to the crypto bros, leaving the established banks and their friends in Washington scrambling to make the barriers to competition even higher. If cryptocurrency is indeed the internet of money, then we are still at quite an early stage of its development. Restrictive regulation in the mid 1990s might have strangled in its infancy the commercialization of the world wide web. Restrictive regulation of crypto could turn out to be a very expensive mistake.

Andreessen-Backed 5G Blockchain Firm Helium Raises $111 Million

Helium Inc., a decentralized peer-to-peer 5G wireless network firm, has raised $111 million in a token sale led by Andreessen Horowitz.

The transaction was structured as a purchase of Helium’s native token, HNT, and included participation from Ribbit Capital, 10T, Alameda Research and Multicoin Capital, according to a statement. The native token is structured to give incentives for the expansion of Helium’s 5G network that provides internet access.

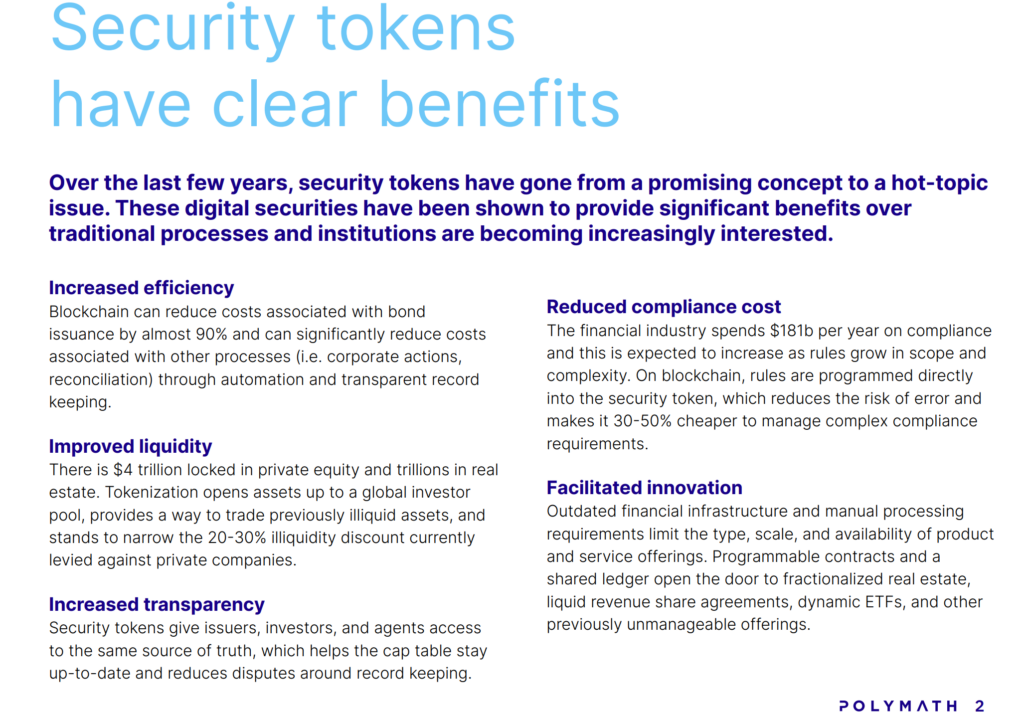

What Needs to Happen for Broader Security Token Adoption

What needs to happen for broader security token adoption

Industry experts weigh in

By POLYMATH

Mini-book-Security-token-adoption

This is not investment advice and should not be considered a recommendation to purchase any crypto-assets.

Full disclosure: I own PolyMath tokens.

Reports of Amazon’s Crypto Plan

“It begins with Bitcoin. This is the key first stage of this crypto project, and the directive is coming from the very top… Jeff Bezos himself.”

Though Amazon is not the first company to add a Bitcoin payment method, it is certainly the most influential one. It operates the top e-commerce store globally with hundreds of millions of people as its customers.

“This entire project is pretty much ready to roll,” the insider added, adding that the company has been working on it since 2019. After Bitcoin, Amazon also has plans to add Ethereum, Cardano, and Bitcoin Cash for payments.

Goldman Sachs: 18% of World’s Super Rich See Crypto as Inflation Hedge

Of the family offices that responded to the survey, 22% had $5 billion in assets under management, and 45% managed between $1 billion and $4.9 billion.

Goldman Sachs’ survey arrived a couple of months after it published a research report which concluded that cryptocurrencies are a legitimate asset class. In May, the bank declared: ”Clients and beyond are largely treating [Bitcoin] as a new asset class, which is notable—it’s not often that we get to witness the emergence of a new asset class.”

https://decrypt.co/76598/goldman-sachs-18-worlds-super-rich-see-crypto-inflation-hedge

JPMorgan Reportedly to Allow Clients to Access Crypto Funds

JPMorgan has reportedly become the first large US bank to allow its financial advisors to give wealth management clients access to cryptocurrency funds.

The bank told its advisors in a memo earlier this week that, as of July 19, they can buy and sell five crypto funds on behalf of a client, Business Insider reported.

The offerings include Osprey Funds’ Bitcoin Trust (OBTC), as well as four from Grayscale Investments: its Bitcoin Trust, Bitcoin Cash Trust, Ethereum Trust and the Grayscale Ethereum Classic Trust.

https://blockworks.co/jpmorgan-reportedly-to-allow-clients-to-access-crypto-funds/

Brazil approves Latin America’s first Ethereum ETF

“QETH11 follows the same Ethereum index used by the CME Group, the CME CF Ether Reference Rate. For this, the ETF buys physical Ethereum and carries out custody with transparency and security for you“, QR said in a statement.

This means that investors seeking to buy Ethereum without direct exposure to the actual cryptocurrency can now do so via this ETF, using any supported brokerage provider.

QR Asset Management will manage the ETF, which the firm says will benefit from Gemini’s “secure institutional custody”. Gemini is a US crypto exchange and custody provider that has previously sought and failed to convince the US SEC to approve their application for a Bitcoin ETF.

The approval of the two ETFs—first BTC and now ETH points to Brazil’s continued support for crypto assets, adding to the clarity within its regulatory environment.

https://coinjournal.net/news/brazil-approves-latin-americas-first-ethereum-etf/