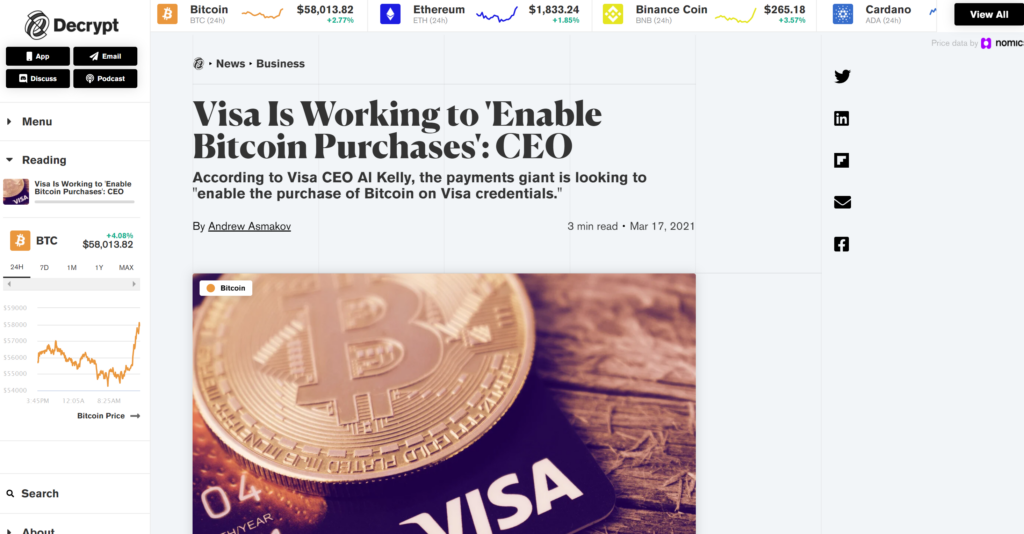

https://decrypt.co/61738/visa-is-working-to-enable-bitcoin-purchases-ceo

Successful Strategies in a Dynamic World Covering Equities, Bitcoin and Crypto-Assets

Baucus will guide the crypto exchange in its dealings with U.S. regulators.

https://www.fool.com/investing/2021/03/05/companies-collectively-bought-39-billion-bitcoin/

Thank you to the Motley Fool for this article.

In addition to the companies and amounts disclosed in this article, just yesterday, March 8, 2021, two new companies disclosed BTC purchases in the $100 million area and deeper moves into developing/acquiring blockchain solutions. PayPal announced yesterday that they are buying Curv, a digital asset security firm for an undisclosed sum estimated to be between $100 million and $300 million.

https://cointelegraph.com/news/paypal-purchases-crypto-custody-firm-curv

Keep your seatbelts on.

December 8, 2020 6:00 PM MicroStrategy goes after more Bitcoin with a new filing to raise $400 million in debt to fund the purchase of additional Bitcoin. This is in addition to the $50 million from Friday’s 8-K filing.

MicroStrategy Announces Proposed Private Offering of $400 Million of Convertible Senior Notes

December 8, 2020 Listen to Michael Saylor explain why he is adding Bitcoin to his company’s balance sheet

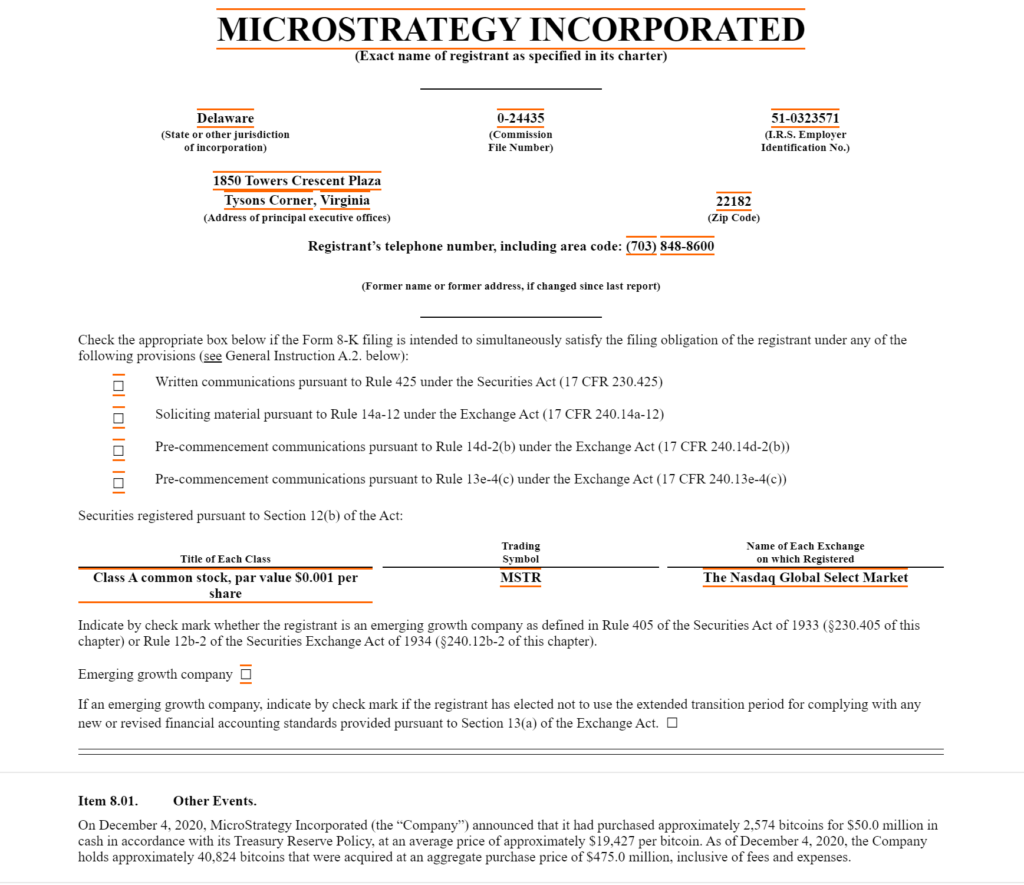

https://www.youtube.com/watch?v=Jb48Q5e4WVgItem 8.01.

Other Events.

On December 4, 2020, MicroStrategy Incorporated (the “Company”) announced that it had purchased approximately 2,574 bitcoins for $50.0 million in cash in accordance with its Treasury Reserve Policy, at an average price of approximately $19,427 per bitcoin. As of December 4, 2020, the Company holds approximately 40,824 bitcoins that were acquired at an aggregate purchase price of $475.0 million, inclusive of fees and expenses.

https://www.sec.gov/ix?doc=/Archives/edgar/data/1050446/000119312520310787/d22733d8k.htm

Many of us have retirement accounts with Fidelity.

They just issued a report on Bitcoin that I believe is very important. If you have the interest to learn about this new asset class that institutions are adopting in investment portfolios, give this a read

</st

My comments appear in this article https://www.netguru.com/blog/fintech-positive-lockdown-effects?hs_preview=AFrlkBri-34009131929