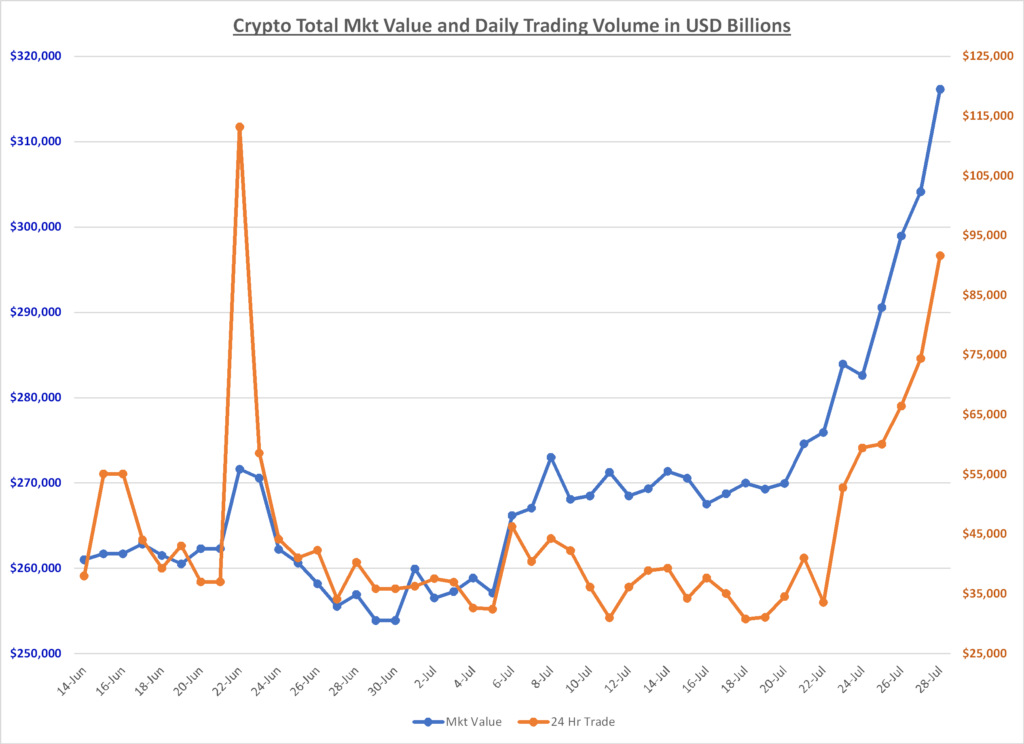

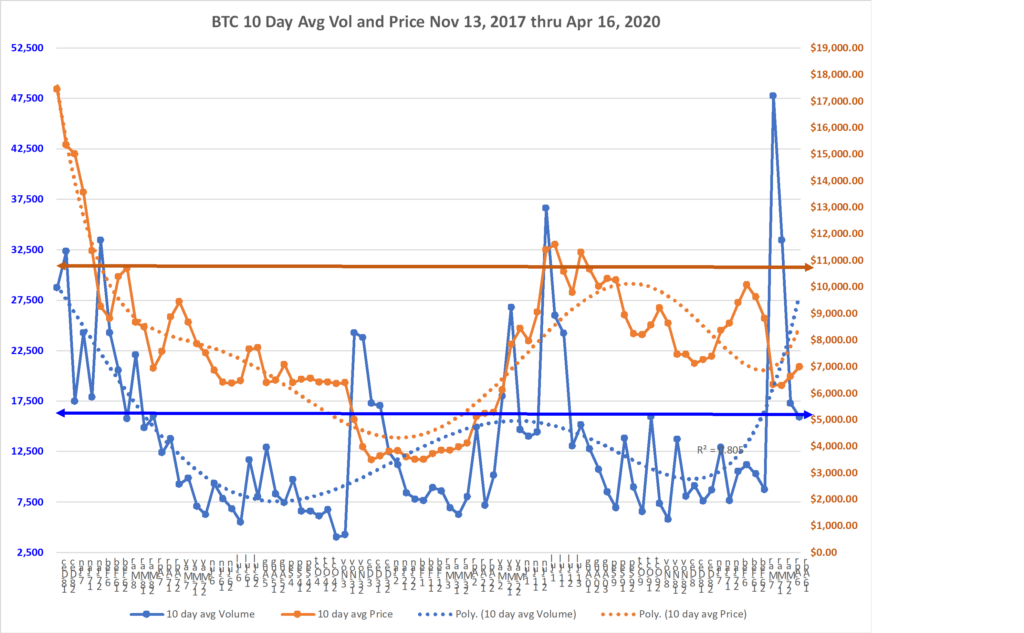

The majority of my research and analysis of late has been very focused on the Crypto-Asset sector. Equities hold little interest for me at the current valuations, which entirely reflect inflation due to Central Bank actions in regard to interest rates and money printing.

Within the Radar Fund tab above, I will post numerous charts to help explain the strength and growth in the Crypto sector. This growth has resulted in the Radar Fund posting a 184% gain YTD.

I am discussing Crypto here on the main page of my website because of the importance of the 2020 developments that extend well beyond the two main Blockchains of Bitcoin and Ethereum. Both BTC and ETH have had great years so far in regard to price growth, demand and broader participation. While this is very good news, the real story of the year is the expansion of business platforms using Blockchain technology to expand commerce and efficiency in many industries. This growth is demonstrated by the following:

1) The Radar Fund holds financial interests in 101 companies/platforms beyond BTC, ETH and LTC. The investment cost of these 101 holdings is a function of the current value of BTC and ETH, the two currencies used to purchase the financial interests in them. As the price of BTC and ETH rise, the cost of acquisition for the other tokens also rises as the current price of BTC and ETH are used to measure the purchase cost rather than the historical prices in effect at the time the other tokens were purchased. This daily real-time mark-to-market of acquisition cost when compared to the current market values of the 101 tokens purchased provides insight as to which platforms are growing faster or slower than the two main Crypto Blockchains of BTC and ETH. By performing this exercise daily and tracking results over time, I believe I am better at identifying the most valuable and accelerating growth businesses in the Crypto sector. The comparison additionally gives me a barometer of overall industry growth. If the basket of 101 tokens that form the Radar Fund industry component are generating price expansion faster than BTC and ETH it demonstrates investment money is flowing into industry faster than it is flowing into Crypto-currencies for holding purposes. To date, as of August 9, 2020, the industry component of the Radar Fund has grown above and beyond BTC and ETH by 39.22%. This industry growth is a key component of the overall YTD return of the Radar Fund’s exceptional 184% growth.

2) The significant and consistent expansion in the number of Bitcoin and Ether Wallets/Addresses further demonstrates the increased penetration and adoption of crypto. YTD, Bitcoin wallets have increased by 17%, and are projected to end the year with a total increase of 27%. YTD, ETH wallets have increased by 46%, and are projected to end the year with a total increase of 62%.

3) Institutional participation in the Crypto sector is expanding as measured by the growth in the use of Futures to hedge and meet obligations in crypto denominated transactions. Futures contracts Open Interest for BTC has reached approximately $5 billion, while Open Interest contracts for ETH approximate $1.5 billion. These are all-time highs in Futures activity Open Interest and demonstrates the growing acceptance and use of Crypto-currencies in the deal making and trading markets.

The array of businesses and industries that are represented by the Radar Fund holdings range from banking, insurance, hedging, travel and leisure, art, market place trading, identity and fraud protection, exchanges, media & entertainment, supply chain management and provenance, education, health, and each day the list expands. It is clear that the use of Blockchains as a technology platform for reducing costs and empowering parties to transact through direct peer-to-peer connections that execute based on established contracts that do not require middle-men to approve, oversee or control the contractual compliance is a better way of doing business in our digital world.

A new day is dawning.